Your hearing is coming up. Your paychecks don't look anything like a normal salary. One month you close several deals and your commission hits hard. The next month is thin because contracts fell through, loans didn't fund, or clients pushed decisions into the next quarter. Now you're trying to figure out child support for commission based income texas, and the standard calculator feels too simple for the way you get paid.

That anxiety is justified. Commission income creates two immediate problems in a Texas child support case. First, the court won't look only at your base salary if commissions are part of your compensation. Second, the primary fight usually isn't whether commissions count. It's how the court turns irregular earnings into a monthly number that can support a binding order.

In practice, that's where cases are won or lost. The parent who walks into court with organized pay records, commission statements, tax returns, and a clear explanation of earning patterns usually has the stronger position. The parent who relies on one recent bad month, rough estimates, or vague testimony usually doesn't.

Texas law gives the framework. Courtroom results depend on evidence and presentation. If you earn through sales, real estate, lending, recruiting, brokerage, or any other commission-heavy role, you need a strategy that matches how judges review variable income.

Introduction

A common client problem looks like this. A sales executive has a modest base salary and a large commission component. During strong months, income jumps. During slower periods, it drops sharply. By the time child support is being set or modified, that parent is asking the same question almost everyone in this position asks: “Will the court use my last paycheck, my annual average, or something else?”

The short answer is that Texas courts are trying to reach a reliable monthly number, not reward or punish one unusually good or bad month. That matters whether you are the parent paying support or the parent trying to prove the other side earns more than they admit.

Commission cases also create practical disputes you don't see in straight-salary cases. A year-end bonus may hit all at once. A chargeback may reduce later checks. A lender may receive incentive pay in bursts. A real estate agent may have a seasonal pipeline. None of that takes the income out of the child support analysis, but it does affect how you should document it.

Courts want a number they can defend with records. They are far less interested in anyone's feelings about whether a commission month was “typical.”

If you're preparing for court, focus on three things early. Gather the full compensation record. Understand how Texas defines net resources. Be ready to explain, with documents, why a particular averaging period reflects reality better than a snapshot.

The Legal Foundation How Texas Defines Income for Child Support

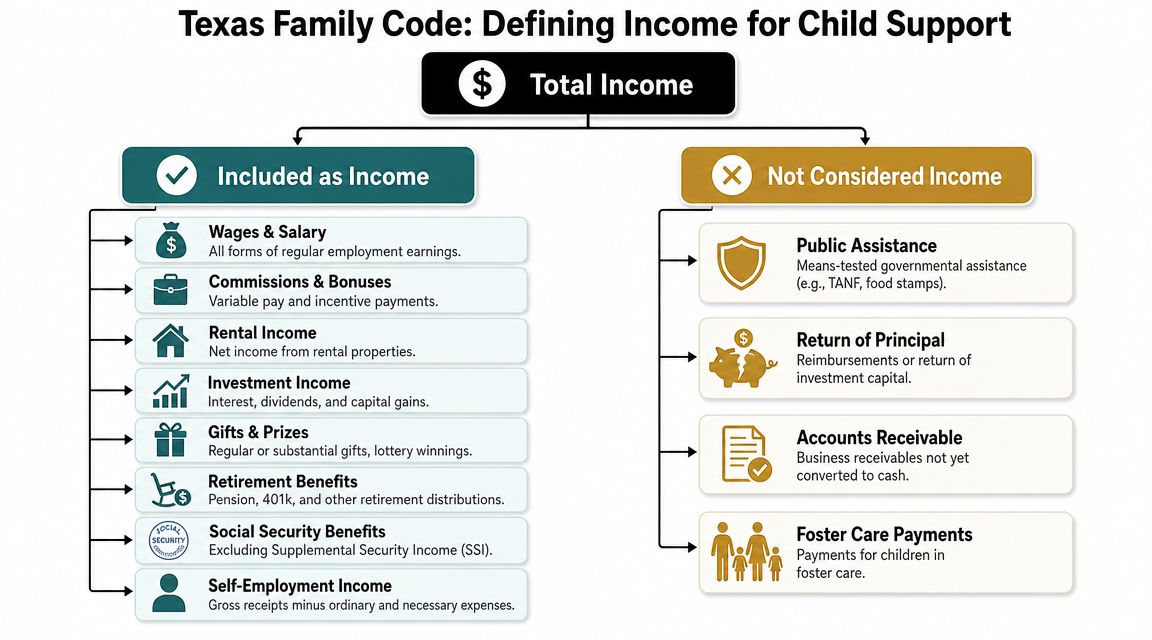

Texas child support starts with net resources, and that term carries significant weight. The governing framework appears in Chapter 154 of the Texas Family Code, especially §154.062 and §154.125. If you earn commissions, the critical point is simple: Texas does not treat commissions as a side category that can be ignored. They are part of the income analysis.

What the court counts

Under the Texas approach, child support begins with broad income sources and then moves to limited deductions. The Texas Attorney General's calculator and Texas Law Help both reflect that commissions are part of the support base, along with wages, bonuses, tips, and other earnings included in monthly net resources, with only certain deductions allowed, such as taxes, union dues, and qualifying health insurance or medical support costs for the child, as summarized by Texas Law Help's discussion of child support and lower incomes.

The practical effect is straightforward. If your employer pays you a base plus commissions, the court is not going to calculate support on the base alone unless the evidence shows the commissions are not part of your recurring compensation picture. In most cases, they are.

For a fuller breakdown of how Texas courts approach the net-resource analysis, review this explanation of how Texas courts calculate net resources.

What gets deducted and what does not

Texas Family Code §154.062 allows a limited set of deductions in reaching net resources. That usually includes the categories reflected in the Attorney General calculator guidance: Social Security taxes, federal income tax, union dues, and certain health-insurance costs for the child.

Practical rule: Commission earners often overstate deductions. Car payments, personal debt, lifestyle expenses, and ordinary household bills do not reduce net resources just because they're real expenses.

That mistake shows up often with loan officers, sales reps, and self-employed producers who blend business spending with personal spending. The court is looking for legally recognized deductions, not a general fairness adjustment.

Why this matters in court

The legal standard matters because it changes the conversation. The issue usually isn't “Do commissions count?” They do. The issue is how reliably they can be measured and whether the proposed monthly figure reflects the parent's actual earning history.

If you are the paying parent, your job is to present a complete income record and a credible averaging method. If you are receiving support, your job is often to prove the other parent's commissions are regular enough to belong in the monthly support base.

That is the foundation of child support for commission based income texas. Everything else is math, evidence, and persuasion.

From Fluctuating Pay to a Fixed Number Calculating Net Resources

The hardest part of these cases is converting irregular income into one monthly figure the judge can place in an order. Texas Law Help confirms the underlying problem. Child support is based on net income from sources that include wages, overtime, tips, bonuses, commissions, and self-employment income, but the consumer materials do not tell you exactly how a court will average irregular commission income, and the official calculator is limited to a single source of income and warns the court-approved amount may differ, as noted in Texas Law Help's child support overview.

What courts usually want

Judges usually want a monthly number that reflects earning reality over time. They generally don't like cherry-picked snapshots. If your income swings because commissions land irregularly, a single pay period can be misleading in either direction.

That is why historical records matter so much. In most commission cases, lawyers and courts work backward from records such as:

- Detailed pay stubs showing year-to-date gross income

- Commission reports from the employer or platform

- Annual compensation summaries that separate base pay, commissions, and bonuses

- Tax returns and attachments if they help confirm broader earnings patterns

- Bank records if deposits help trace actual compensation received

Common averaging approaches

No one formula fits every case, but these are the methods that tend to come up in real hearings.

Recent annual average

This is often the cleanest method when the parent has a stable role and consistent commission structure. The court looks at a broad period and calculates an average monthly gross amount before applying allowable deductions.

This approach works well when the earning pattern is seasonal. It tends to smooth out one exceptional month and one weak month.

Year-to-date method

Sometimes the evidence set is limited, or the current year tells the most accurate story because compensation structure changed. A year-to-date calculation can be useful, but it becomes less persuasive if the period is too short or if the highest commission months haven't happened yet.

If you're arguing year-to-date, you need a reason. New compensation plan. New territory. Recent employer change. Documented shift in market conditions. Without that context, the judge may prefer a broader look.

Here is a short way to consider it:

| Method | When it helps | Where it fails |

|---|---|---|

| Broader historical average | Stable role with seasonal variation | Can understate a recent permanent income drop |

| Year-to-date average | Recent compensation change with records | Can distort income if the year is incomplete |

| Single recent month | Rarely persuasive except in unusual cases | Usually too volatile to trust |

A useful video overview of Texas child support mechanics is below.

What works and what does not

I'll put this plainly because it matters. Saying “my income fluctuates” is not a strategy. Proving the pattern is.

What works:

- Clean records over time. If you have full pay and commission statements, your lawyer can usually build a defensible average.

- Explaining anomalies. If one quarter was inflated by a one-time payout or depressed by a documented clawback, identify it and support it.

- Matching the averaging period to the facts. Courts respond better when the method fits the compensation structure.

What usually fails:

- Relying on one bad month.

- Presenting only tax returns when current pay records tell a different story.

- Asking the court to ignore commissions because they are unpredictable.

Variable income does not make support impossible to calculate. It makes documentation more important.

The Guideline Formula and the New $11,700 Cap

A commission earner can have two strong months, one weak month, and still end up with a child support number that feels surprisingly fixed. That is how the guideline system works in Texas. Once the court settles on monthly net resources, the percentage formula in Texas Family Code §154.125 applies the same way it would for any other parent.

For commission income, the principal advantage is not in arguing over the percentage. It is in making sure the court is using a fair monthly average before that percentage is applied.

The percentage schedule

Texas uses a guideline schedule tied to the number of children before the court under §154.125. In a standard case, the court applies 20% for one child, 25% for two, 30% for three, 35% for four, and 40% for five, with not less than 40% for six or more children.

That sounds simple. In commission cases, it rarely feels simple because the percentage is often the easy part. The harder question is whether the judge should use a twelve-month average, a year-to-date average, or a longer period that smooths out a seasonal sales cycle. By the time the court reaches the formula, the income fight has usually already been won or lost.

The cap effective September 1, 2025

For cases governed by the current law, Texas raised the cap on monthly net resources used in the guideline calculation to $11,700 effective September 1, 2025. If the paying parent's monthly net resources fall at or below that amount, the court typically applies the guideline percentage directly to that figure.

If the paying parent's net resources are above the cap, the guideline amount is usually calculated only on the first $11,700. That does not end the analysis. It sets the baseline.

For a practical explanation of how the updated limit works, see this guide to the Texas $11,700 child support cap.

High-commission cases often turn on this point. A sales executive may have months that are far above the cap and months that fall well below it. The court still needs a defensible monthly number, and the averaging method matters because it determines whether the case stays within the capped guideline calculation or opens the door to an above-guideline dispute.

When courts go above the guidelines

Texas Family Code §154.123 allows the court to vary from the guidelines when the facts justify it. In above-cap cases, the argument usually shifts to the child's proven needs and the evidence supporting them.

That is where parties make expensive mistakes.

A commission earner who argues only, “my income is capped,” can miss the core issue if the other side has organized proof of additional needs. The receiving parent can make the opposite mistake by asking for more support without records showing those needs in a concrete way. Judges usually want specifics: tuition, therapy, uninsured medical costs, tutoring, transportation, or other expenses tied to the child, not broad claims that a higher earner should just pay more.

In practice, once income rises above the cap, these cases become less about the formula and more about evidence quality.

Practical Examples Child Support Calculations in Action

A commission earner closes three large deals in one quarter, then has two slow months. By the time the support case reaches court, one parent says the high months prove strong earning capacity. The other says those checks were unusual and should not set support for the next several years. That dispute is common in Texas. The result usually turns on which side has the better averaging method and the cleaner records.

Example one below the cap

A parent in medical device sales earns a modest base salary and monthly commissions that change with hospital contracts and product cycles. The court's job is to convert that uneven stream into a monthly net-resources figure it can use consistently. In practice, lawyers often start with 12 months of pay records and ask whether that period fairly reflects ordinary earnings. If the compensation pattern is highly seasonal, a longer period may be more accurate.

Assume the records show regular commissions, one unusually large payout tied to a backlog release, and no sign that the spike will repeat. The dispute is usually not about the statutory percentage. The dispute is whether that payout belongs in a straight average, should be weighted differently, or should be explained as a one-time event. A paying parent who labels it “nonrecurring” without backup usually loses that point. A parent who brings the commission statement, employer compensation plan, and prior year trend has a much stronger argument.

If the final monthly net-resources number falls below the cap, the court applies the guideline percentage in §154.125.

Example two above the cap

Now take a software sales executive whose commissions rise and fall with enterprise closings. Some months are ordinary. Others include a quarterly accelerator or year-end true-up that pushes monthly net resources well above the guideline ceiling.

As noted earlier, the current cap for guideline analysis is $11,700 in monthly net resources. If the averaged figure exceeds that amount, the guideline calculation stops at the cap. The court can still consider whether the child has proven needs that support an amount above the guideline level under §154.123.

That creates two separate fights in the same case:

- Averaging fight. What period best reflects actual commission income. Twelve months, twenty-four months, or another span tied to how the job pays.

- Cap fight. Whether the guideline amount should be limited to the capped figure.

- Needs fight. Whether reliable evidence shows the child needs support above the guideline amount.

The practical point is simple. High commission income still matters after the cap, but it matters in a different way. It may shape the court's view of ability to pay, and it may frame the dispute over whether claimed child-related expenses are legitimate, necessary, and tied to the child.

Example three shared possession and offset thinking

Shared possession does not cancel support, especially when one parent earns substantially more and that income includes commissions. In negotiated cases, lawyers often run an offset-style analysis to test settlement positions. Courts still decide support under the Family Code, but this method helps show how each side is valuing the income evidence.

| Calculation Step | Parent A (Higher Earner) | Parent B (Lower Earner) |

|---|---|---|

| Determine each parent's monthly net resources | Use earnings records, including commissions averaged over a defensible period | Use earnings records |

| Apply the guideline percentage for the child or children before the court | Calculate hypothetical support obligation | Calculate hypothetical support obligation |

| Compare the two amounts | Higher obligation identified | Lower obligation identified |

| Offset one against the other | Difference may be proposed as payment | Difference may be received |

This model breaks down fast if one parent uses gross deposits from a strong quarter and the other uses a reduced number pulled from a single slow month. I often see that mistake in early mediation packets. The math looks precise, but the inputs are distorted.

In shared-possession commission cases, the first battle is usually over the averaging period, not the final percentage.

What these examples show

The formula matters less than people expect. The hard part is deciding which earnings history gives the court a fair monthly number.

In a stable salary case, that step is usually easy. In a commission case, it is the whole case. Judges want a number they can defend with records, not a number built around the best or worst month either side can find.

Strategic Documentation Proving Commission Income in Court

Commission cases are document cases. Testimony matters, but paper usually decides whose version of income the court trusts. If you walk into court with incomplete records, the judge may fill the gaps in a way you won't like.

The documents that matter most

Start with the compensation documents that show how you are paid and what has been paid.

The strongest document set usually includes:

- Employment agreement or compensation plan. This shows base salary, commission triggers, bonus eligibility, and clawback language.

- Pay stubs with year-to-date figures. These often expose the annual pace of earnings faster than any testimony can.

- Commission statements. If your employer issues deal-level or monthly reports, bring them.

- Tax records. Useful for confirming the broader earnings picture, especially when the commission structure has been stable.

- Bank statements. Helpful when deposits trace compensation timing or when the other side is understating cash flow.

If you need a practical checklist for a Texas support case, this evidence guide for Texas child support litigation is a useful starting point.

Discovery is where hidden income surfaces

If the other parent's records are incomplete, formal discovery usually matters. In a contested suit affecting the parent-child relationship, or in a modification case, discovery tools can force a more accurate income picture.

Those tools usually include:

- Interrogatories asking the other party to identify all employers, pay methods, bonuses, and commissions

- Requests for Production seeking pay records, commission reports, contracts, and tax material

- Subpoenas directed to employers or financial institutions when necessary

- Depositions that lock a party into sworn testimony about compensation patterns and disputed deductions

One factual option for parents dealing with these issues is the Texas Child Support Law Office of Bryan Fagan, which handles net-resource disputes, modifications, enforcement actions, and high-income child support cases under Chapter 154 of the Texas Family Code.

What to do with clawbacks and chargebacks

Commission earners often ask about clawbacks. The key is proof. If prior commissions were reversed under the compensation plan and later pay was reduced accordingly, bring the plan documents and the later statements showing the reversal.

Don't expect the court to accept a general complaint that “some deals came back out.” Show the deal, the policy, and the accounting trail.

The best evidence in a commission case is usually the evidence generated before anyone filed suit.

That is why organized employer records carry so much weight. They were created in the ordinary course of business, and judges tend to trust them more than after-the-fact summaries prepared for litigation.

Changing Circumstances Modifying and Enforcing Your Order

A child support order isn't frozen forever. For a commission earner, income can change for legitimate reasons. A compensation plan can be cut. A territory can be reassigned. An industry slump can reduce opportunity. A promotion can increase earnings. Texas law allows child support modification when the legal standard is met.

Modification when income changes

Texas courts generally require proof of a material and substantial change in circumstances to modify support. For commission earners, the central issue is whether the change reflects a real shift in earning capacity or a temporary swing that comes with the territory.

That distinction matters. If your commissions have always gone up and down, the court may view a short downturn as normal volatility. If your company changed the compensation plan, eliminated your accounts, or moved you into a materially different role, that is a stronger modification record.

A typical modification process includes:

- Filing a petition to modify the existing order

- Serving the other party

- Exchanging updated financial records

- Attending mediation or a hearing

- Presenting evidence of the changed income pattern

The sooner you act, the better. Waiting while arrears accumulate usually puts the paying parent in a weaker position.

Enforcement when support is not paid

If support is ordered and not paid, Texas courts can enforce the order. The receiving parent may file a motion for enforcement, and the court can use remedies such as wage withholding and other collection tools recognized under Texas law.

For commission earners, enforcement can become especially serious when a parent assumes irregular income excuses irregular payment. It doesn't. The order controls unless it is modified.

Here is the practical rule that avoids most enforcement trouble:

- If income dropped, seek modification promptly.

- If support is unpaid, document every missed amount and every due date.

- If wage withholding does not capture all income sources, expect closer scrutiny.

A parent who keeps paying according to the order while pursuing modification usually looks responsible. A parent who stops paying first and explains later usually doesn't.

Critical FAQs and Final Strategic Advice

How are annual bonuses treated compared to regular commissions

If a bonus is part of your compensation history, it can become part of the income picture the court evaluates. The key question is whether the evidence shows it is recurring, expected, or part of the broader earnings pattern. The label matters less than the payment history.

What if my commissions have clawbacks or chargebacks

Bring the compensation plan and the records showing the reversal. Courts respond to documented accounting adjustments, not general complaints about instability. If the clawbacks materially affect what you received, that needs to be shown clearly.

Can parents agree to their own child support number

Yes, parents can reach agreements, but the court still reviews child support through the lens of the Texas Family Code and the child's best interest. Informal side deals that are not reflected in an enforceable order create problems later, especially in enforcement or arrears disputes.

Does being paid as a 1099 contractor hide commission income

No. Payment form does not make income disappear. If you receive money through commissions, contractor compensation, or self-employment structures, the court can still examine the records to determine net resources.

What matters most before court

Three strategic points usually decide these cases.

First, don't argue from a snapshot when your income is variable. Build the most accurate earnings history you can.

Second, separate legal deductions from ordinary expenses. Many commission earners hurt their credibility by claiming deductions the Family Code does not allow.

Third, treat above-cap cases and modification cases as evidence-heavy cases. The more your income structure departs from a plain salary, the more important your documentation becomes.

If you're dealing with child support for commission based income texas, the court is trying to answer one practical question: what monthly net-resource figure most accurately reflects reality? Bring the records that answer that question, and your case becomes much easier to present.

If you need help establishing, modifying, enforcing, or contesting child support tied to commissions, bonuses, or other variable pay, the Texas Child Support Law Office of Bryan Fagan works with parents across Texas on Chapter 154 child support issues, including net-resource disputes, high-income cases, and 50/50 possession support questions.