If you're self-employed and heading into a Texas child support case, your biggest mistake is thinking your tax return controls the answer. It doesn't. The court isn't deciding what the IRS accepted. The court is deciding what money is available to support your child.

That difference changes everything.

In child support if parent is self employed Texas cases, judges look past labels, deductions, and neat accounting categories. They want the actual income figure. If your income swings month to month, if you run expenses through the business, or if the other parent says you're hiding money, expect a hard look at your records. If you're the parent receiving support, don't accept a low Schedule C at face value. If you're the parent paying support, don't show up with vague spreadsheets and hope for the best.

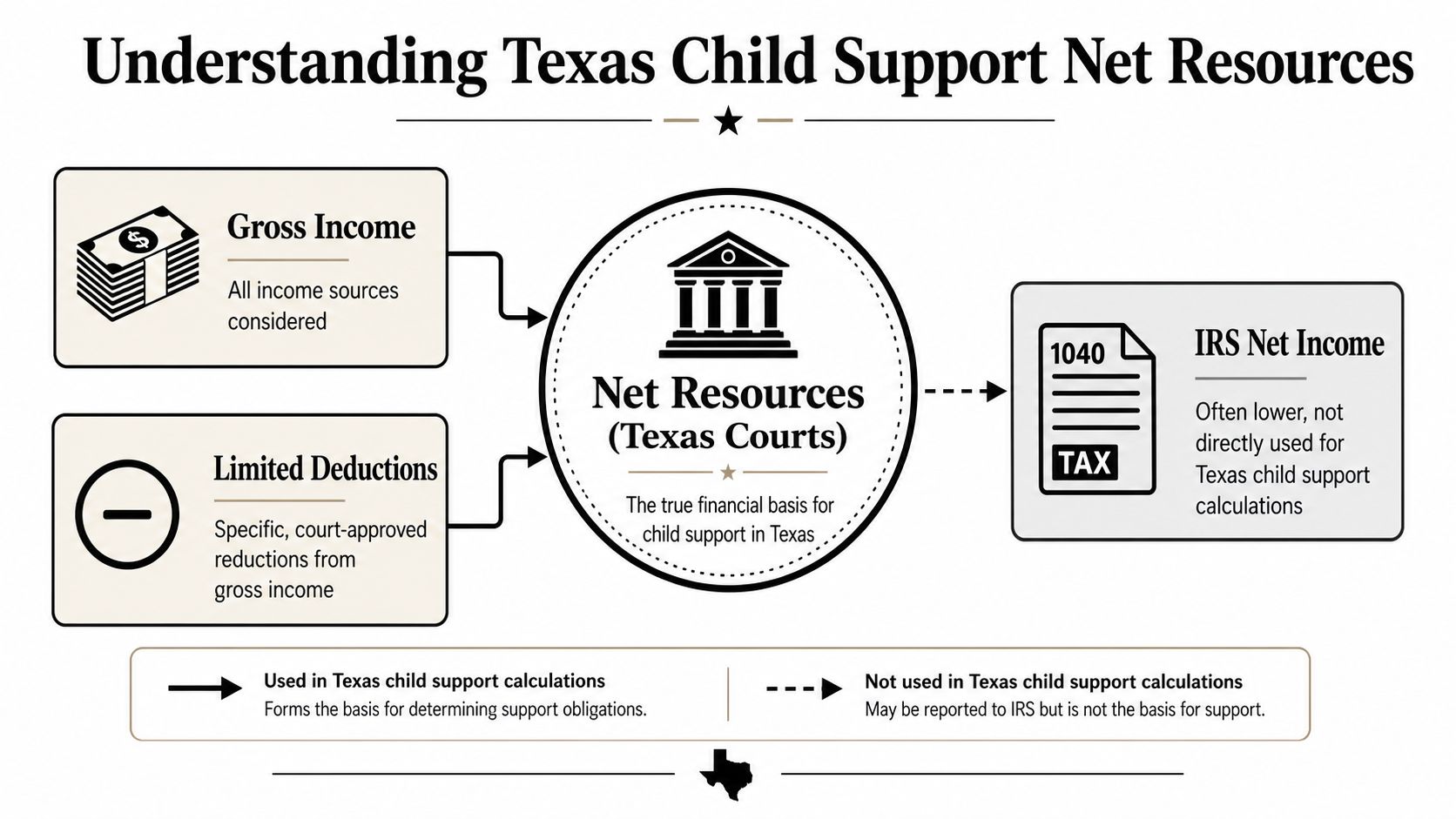

The Foundation of Texas Child Support Net Resources

Texas uses monthly net resources. That is the starting point under Texas Family Code §154.062, not taxable income and not the number you prefer on your return. For self-employed parents, the court starts with gross business income and subtracts only ordinary and necessary business expenses required to produce that income. Texas courts also review a broad financial record and commonly examine 12 to 36 months of income, bank statements, and business documents to stabilize fluctuating earnings, as explained in this discussion of Texas net resources for self-employed parents.

Your tax return is not your courtroom answer

A lot of self-employed parents walk in saying, "My tax return shows very little income." That argument usually falls apart fast. Tax law allows deductions for tax purposes. Family court asks a narrower question. Was the expense necessary to generate income?

That is why your child support calculation often looks different from your accounting records. If you want a useful primer on the concept, review how Texas courts calculate net resources.

Practical rule: If an expense helps you lower taxes but doesn't clearly help you earn business income, expect a judge to question it.

What the court actually reviews

Judges don't like snapshots when the income picture is uneven. They want a pattern. In self-employment cases, that usually means a wider set of records than people expect.

Bring organized proof of:

- Business income deposits: Show what came in, not just what ended up on a return.

- Bank activity: Personal and business accounts often tell a cleaner story than a self-prepared summary.

- Core business records: Invoices, contracts, payment app records, and bookkeeping reports matter.

- Expense backup: Receipts and account statements matter more than your word.

The point is simple. Texas courts want a stable monthly figure. If your income rises and falls, the court may average a longer period rather than rely on the month that helps you most. That is why preparation beats explanation. If your records are messy, the court may assume the mess favors you.

Calculating Guideline Child Support for the Self-Employed

You walk into court claiming you only made $3,000 a month because your tax return says so. The judge looks at your bank deposits, your Venmo history, your credit card statements, and your business account transfers. If those records show more cash than your return reflects, your guideline support will be based on the higher number.

That is how self-employment cases are decided in Texas. The court starts with monthly net resources, then applies the guideline percentages in Texas Family Code §154.125. For self-employed parents, the fight is rarely over the percentage. The fight is over the income figure the court will trust.

The formula the court uses

Once net resources are set, the guideline math is straightforward:

- 1 child: 20%

- 2 children: 25%

- 3 children: 30%

- 4 children: 35%

- 5 or more children: 40%

Those percentages apply to the obligor's monthly net resources, subject to the statutory cap. For cases filed on or after September 1, 2023, the guideline cap is based on the first $11,700 of monthly net resources under §154.125. If proven net resources are higher, the court can consider additional support, but guideline support is calculated on that capped amount unless the evidence justifies more.

How self-employed parents should run the calculation

Use the same sequence the judge will use:

Total the income coming in.

Include business revenue, contract payments, cash jobs, app-based work, commissions, retainers, and side income.Subtract only allowed items to reach net resources.

The court is looking for ordinary and necessary business expenses, along with the deductions Texas law allows in the child support formula.Convert the result to a monthly number.

If income is irregular, expect the court to average it over time instead of accepting a single strong or weak month.Apply the guideline percentage.

The percentage is fixed by the number of children before the court.Check the cap.

If monthly net resources exceed $11,700, guideline support stops there unless the other side proves the child's proven needs support a higher amount.

This sounds mechanical. In a courtroom, it is not. A self-employed parent with clean books and believable expense records usually gets a better outcome than a parent who shows up with a tax return and excuses.

A simple example

Assume the court finds a self-employed electrician has $4,800 in monthly net resources after allowing legitimate business expenses. If there is one child before the court, guideline support is 20%, or $960 per month.

Now assume monthly net resources are $12,500 for that same parent. For guideline purposes, the court applies the percentage to $11,700, not the full $12,500. With one child, guideline support would be $2,340 per month, before any argument about proven needs above the cap.

That cap matters. So does the paper trail behind the number.

What usually changes the result

Self-employed cases turn on proof, not labels. Calling yourself a business owner does not reduce support. Writing off personal spending does not reduce support. Large depreciation entries on a return do not automatically reduce support either.

Judges want a usable monthly number they can defend from the bench. If your records are inconsistent, expect the court to rely on bank activity, deposit patterns, prior returns, and year-to-date business records to build its own number. For a practical breakdown of the math itself, review this guide on how to calculate child support in Texas.

Disputed Business Deductions and Income Add-Backs

At this point, most self-employed parents lose credibility.

Texas courts don't automatically accept a claimed business deduction just because your accountant booked it that way. Personal expenses deducted for tax purposes, including personal vehicle use, non-business meals, and excessive home office costs, are routinely added back into income. Judges also frequently average 3 to 5 years of business records to smooth income and prevent manipulation, as described in this Texas discussion of lower incomes and self-employment scrutiny.

What add-backs mean in plain English

An add-back is simple. You deducted the expense in the business. The court decides it wasn't necessary for generating income. The court puts that money back into your income stream for child support purposes.

That issue comes straight out of Texas Family Code §154.062. The statute allows ordinary and necessary business expenses. It does not give you a free pass to run personal living costs through the company and reduce support.

The expenses judges challenge first

If you're preparing for a hearing, assume these categories will get attention:

- Vehicle costs: A work truck used only for business is easier to defend than a family SUV used for both errands and client meetings.

- Meals and entertainment: A real client meeting may be defensible. Routine personal meals are not.

- Travel: Travel directly tied to work is one thing. Family trips labeled "business development" are another.

- Home office claims: A legitimate dedicated workspace may survive scrutiny. Inflated home-related costs usually won't.

- Mixed-use items: Phones, internet, fuel, and equipment often require a clear allocation between business and personal use.

If you can't show why the expense was necessary to produce income, the court has every reason to treat it as money available for support.

Common Business Expense Rulings in Texas Child Support Cases

| Expense Category | Typically Allowed (if properly documented) | Typically Disallowed or Added Back |

|---|---|---|

| Vehicle expense | Business-only use tied to actual work activity | Personal driving, commuting, family use |

| Meals | Genuine business meeting expense | Personal meals or loosely described food charges |

| Travel | Travel required for client work or operations | Vacations or mixed personal trips |

| Home office | Reasonable, business-specific portion | Excessive or poorly documented home costs |

| Equipment and tools | Items directly used to perform work | Purchases with substantial personal use |

| Phone and internet | Business allocation supported by records | Full deduction when use is mixed and undocumented |

How to prepare if deductions will be attacked

Don't argue in labels. Argue in documents.

Use this checklist:

- Separate accounts: If you mix personal and business spending, you make the other side's job easy.

- Match receipts to revenue: Show how the expense helped produce business income.

- Fix weak categories early: If a charge looks personal, don't build your whole case around defending it.

- Expect discovery: The other parent can seek tax returns, bank statements, bookkeeping records, invoices, and account statements.

- Prepare for underreporting claims: If your lifestyle looks expensive compared to your reported income, you need an answer backed by paper.

If you're on the receiving side and you suspect gamesmanship, review how underreporting income affects Texas child support disputes. That issue often drives the entire case.

How Texas Courts Impute Income

A low reported income doesn't end the inquiry. If your numbers don't match your life, the court can decide you're capable of more and calculate support accordingly. That is the practical force behind imputed income in self-employment cases.

Reported income is only part of the picture

Texas courts may impute income when a parent's reported earnings are inconsistent with lifestyle or spending patterns. The verified guidance on self-employed child support in Texas explains that courts can treat the discrepancy as additional available income for support purposes.

That means a judge may look at the whole record and ask a hard question: if you say you earn very little, how are you paying for everything else?

Relevant proof can include:

- Past earnings history

- Education and skills

- Business gross receipts

- Personal and business bank activity

- Spending patterns that don't fit the claimed income

When underemployment looks intentional

Self-employed parents sometimes reduce salary, delay invoicing, increase questionable write-offs, or claim a sudden downturn right before court. Judges see that pattern often enough to be skeptical.

If you're paying support, don't assume a lean year will be accepted without context. If you're receiving support, don't accept "the business is slow" as a complete answer when deposits and spending suggest otherwise.

A short explainer may help if you're preparing for this issue:

Courts don't have to believe a self-employed parent's spreadsheet when the bank records and lifestyle tell a different story.

Real-World Examples and Complex Scenarios

The law gets clearer when you run the numbers. These examples show how courts tend to approach self-employed cases under §154.125 and, when needed, deviations under §154.123.

Example one with a standard self-employed contractor

A contractor presents reliable books. The court accepts the business expenses and determines monthly net resources are $6,000. There is one child before the court.

Under §154.125, the guideline percentage is 20%. The guideline child support amount is $1,200.

This is the easy case. Clean records. Consistent earnings. No serious add-back fight.

Example two with fluctuating income and the new cap

Most online articles often fail people.

For self-employed parents with volatile earnings, courts may average income over different periods, including 3, 12, or 24 months, to decide whether the monthly average exceeds the updated $11,700 net resource cap effective September 1, 2025, as discussed in this Texas child support cap overview. If the averaged monthly net resources are above that cap, the standard guideline percentages apply up to the cap. Any support above that point requires a needs-based analysis under §154.123.

Here is the practical effect.

Assume a business owner has several strong months and several weak months. One side wants the court to average only the recent strong stretch. The other side wants a longer average that includes seasonal dips. The averaging period can decide whether the parent's monthly average is over the $11,700 cap or below it.

If the average stays below the cap, the court applies the normal guideline percentage to the full averaged net-resource number. If the average exceeds the cap, the guideline percentage applies to the capped amount, and then the court considers whether the child's proven needs justify more under §154.123.

Courtroom advice: In a fluctuating-income case, the fight is often not over the percentage. It's over the averaging period.

Example three with near-equal possession

Texas doesn't automatically cancel child support because parents share time closely. In some cases with a near-equal schedule, lawyers and courts use an offset-style approach. Each parent's guideline obligation is calculated, then the higher-earning parent pays the difference.

A simplified example helps. Parent A has monthly net resources of $6,000. Parent B has monthly net resources of $4,800. There is one child. Parent A's guideline amount is 20% of $6,000, which equals $1,200. Parent B's guideline amount is 20% of $4,800, which equals $960. The difference is $240, so Parent A may pay that offset amount if the facts and order structure support it.

That is not automatic in every case. The court still looks at the conservatorship structure, the child's needs, and whether a deviation under §154.123 makes sense.

The Legal Process for Your Child Support Case

You walk into court with a clean tax return, a thin profit and loss statement, and no backup for the deductions. The other side walks in with bank records, Venmo transfers, credit card statements, and photos showing a lifestyle your reported income cannot support. That hearing is usually decided before anyone testifies.

Self-employment child support cases are document cases first and credibility cases second. If your records are sloppy, the judge has room to reject your numbers, add back expenses, and set support from a higher income figure than the one on your return.

How a Texas case usually moves

A Texas child support case involving a self-employed parent usually follows this path:

File the case or the modification.

The case may be part of a divorce, a SAPCR, or a petition to modify an existing order.Get service right.

Bad service causes delay, resets hearings, and gives the other side procedural arguments you do not need.Exchange financial information.

Expect requests for tax returns, bank statements, profit and loss statements, general ledgers, 1099s, invoices, QuickBooks reports, and business account records. In a self-employment case, a bare tax return rarely settles the issue.Use formal discovery early if the income story does not add up.

Ask for underlying business records, not summaries. If a parent claims low income but the deposits are high, the deposits matter. If the parent claims large write-offs, the receipts and account statements matter.Prepare for mediation as if it were trial.

Mediation goes well when you can prove your numbers. It goes badly when you rely on broad estimates and unsupported deductions.Build the hearing file by issue.

Separate your exhibits into income, claimed deductions, personal expenses paid through the business, bank deposits, cash withdrawals, and credibility problems. Judges follow organized proof.

What the court is actually deciding

The legal question is not whether a parent is "self-employed." The legal question is what counts as net resources under Texas Family Code Chapter 154 and what monthly amount the court should use for guideline support.

That is why these hearings often turn on a few practical points:

- whether the records are complete

- whether business deductions are necessary to produce income

- whether personal expenses were run through the business

- whether income should be averaged over time

- whether the court should disregard the reported income and impute a higher amount

A judge does not have to accept a tax return at face value. In a disputed case, the court compares the return to the actual money flow.

Modification cases require proof

If you want to change an existing order, prove the legal basis for modification. In many cases, that means a material and substantial change since the last order. For a self-employed parent, that usually means one of four things. The business income changed. The business structure changed. The parent now has better records than before. Or the other side uncovered financial information that was missing the first time.

Bring old and new records that show the change clearly. Do not rely on a general claim that business is "down this year." Judges want dates, monthly figures, account statements, and a clean comparison between then and now.

What wins these cases

Win the paper war.

Use a hearing binder or electronic exhibit set that lets the judge see the issue fast. If you are claiming a deduction, tie it to a specific business purpose and supporting record. If you are attacking a deduction, show the personal use. If you are arguing hidden income, trace deposits, payment app transfers, or repeated personal spending inconsistent with the claimed income.

In self-employment cases, the side with the cleaner records usually has the stronger child support number.

Frequently Asked Questions for Self-Employed Parents

Can the court use an average if my income is seasonal

Yes. In self-employment cases, that is often the sensible approach. If your business has strong and weak seasons, bring enough records to show the pattern. A cherry-picked month won't help you much.

Can I deduct my car, meals, or home office

Sometimes. But only to the extent the expense is legitimately tied to producing income and you can prove it. If the expense has a personal component and your records are weak, expect an add-back argument.

What if the other parent runs a cash business

Focus on bank deposits, payment app records, invoices, lifestyle evidence, and business activity that doesn't line up with the reported income. Cash businesses are exactly where discovery matters most.

Do gig jobs count as income

Yes. Texas guidance recognizes that resources include gig economy income. If the parent drives, delivers, freelances, or takes app-based contract work, that income belongs in the child support analysis.

What happens if the judge thinks I'm hiding income

You lose credibility fast. Then the court may reject claimed deductions, average a longer income period, or impute income based on earning capacity and spending patterns. Once the judge doubts your numbers, every issue gets harder.

Does equal custody mean no child support

No. A close possession schedule does not automatically eliminate support. The court may still order support, and in some cases an offset-style analysis becomes part of the argument.

What should I bring to the hearing

Bring organized financial records, not a stack of excuses.

That usually means:

- Tax returns and schedules: Especially business-related schedules.

- Profit-and-loss reports: Clean, readable, and consistent with the bank records.

- Bank statements: Personal and business if the issues overlap.

- Invoices and contracts: Show how money was earned.

- Proof for contested expenses: Receipts, statements, and a clear explanation of business necessity.

Should I settle or force a hearing

Settle if the numbers are honest and the order is workable. Force a hearing if the other side is gaming income, inflating deductions, or refusing to produce records. In self-employment cases, bad paper often deserves judicial scrutiny.

If you're dealing with self-employment income, disputed deductions, a modification request, or a hearing over hidden earnings, the Texas Child Support Law Office of Bryan Fagan can help you prepare the financial record, challenge weak income claims, and present a support calculation that matches Texas law.